Take a look at the inventory journal entries you need to make when manufacturing a product using the inventory you purchased. If you sell products at your business, you likely have some form of inventory. Knowing how much inventory you have on hand, as well as how much you need to have steps for reconciling irs form 941 to payroll in stock, is a crucial part of running your business. To help keep track of inventory, you need to learn how to record inventory journal entries. As inventory is sold, the Merchandise Inventory account is credited, and Cost of Goods Sold is debited for the cost of the inventory sold.

Journal Entry Types for Small Businesses

The management needs to provide a high rate of provision for such kind of inventory as they have a high rate of loss due to damage or obsolete. Businesses with high transaction volumes or those that need daily oversight of their finances should record entries daily. Weekly is good for moderate transaction volumes, and monthly works for most businesses with low transaction volumes. This entry records the consignment inventory on the retailer’s books, acknowledging that the goods are not owned by the retailer but still need to be accounted for. By undertaking regular inventory valuations, you can build an accurate picture of your business’s inventory and how much it really costs. It’s important to identify any indirect production cost, allowing you to create a complete budget that includes all the expenses related to your inventory.

Accounting made easy, for FREE!

Depending on the size and complexity of the business, a reference number can be assigned to each transaction, and a note may be attached explaining the transaction. For example, the inventory cycle for your company could be 12 days in the ordering phase, 35 days as work in progress, and 20 days in finished goods and delivery.

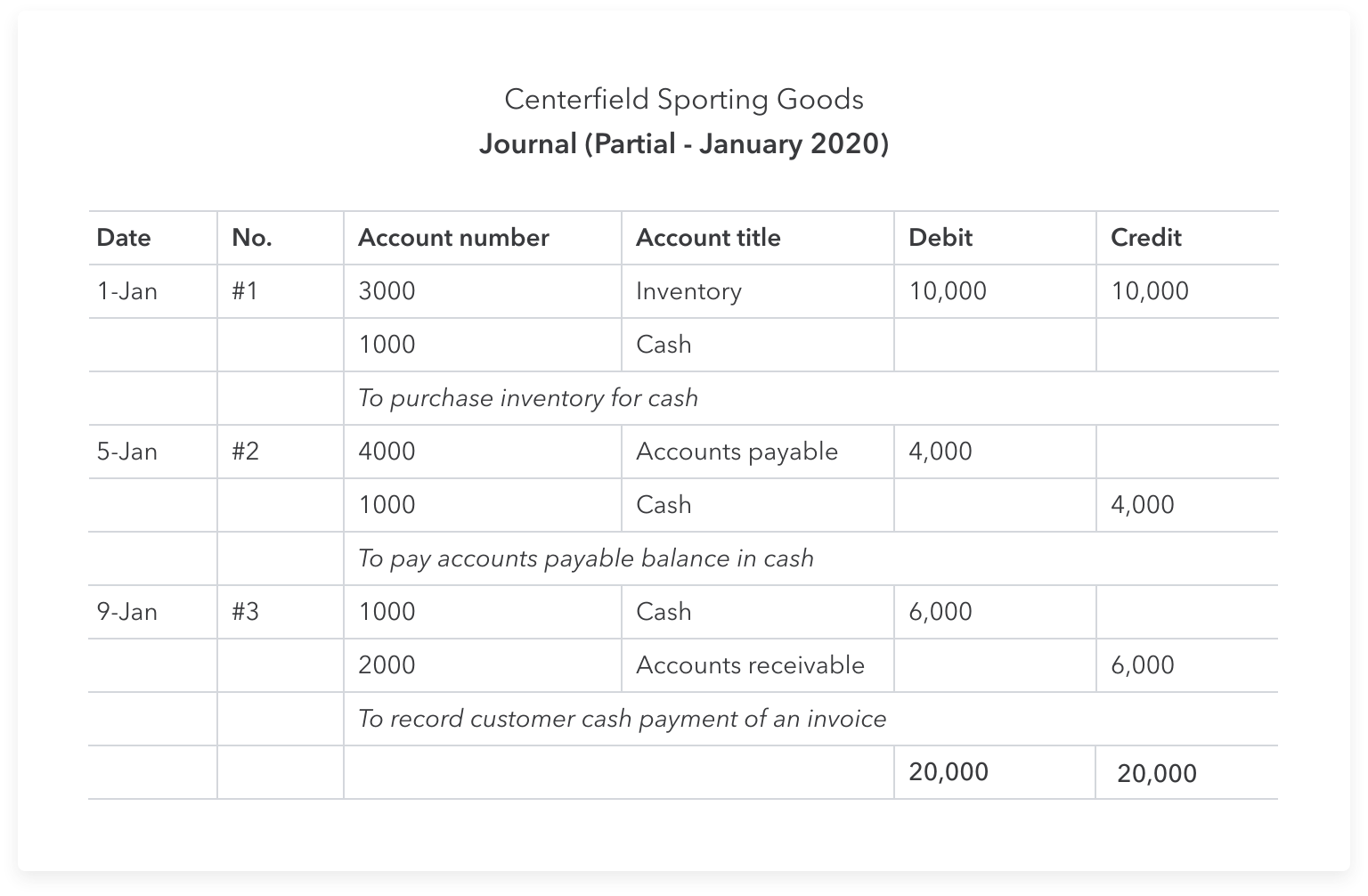

Perpetual inventory system

Sales transaction entries record any profits from the sale of finished goods. The COGS inventory accounting journal entries are your beginning inventory plus purchases during the accounting period, minus your ending inventory. COGS are only recorded at the end of an accounting period to show inventory sold. Unlike the perpetual inventory system, there is no cost of goods sold account or the inventory account in the above journal entry. This is due to, under the periodic system, the company does not record the cost of goods sold nor make any update to the inventory balances on the date of sale.

- Let’s assume that a firm has started its year with a beginning inventory of pens costing $10,000.

- Both shrinkage and obsolescence negatively impact the company’s financial performance by increasing COGS and reducing profitability.

- One common mistake in inventory management is overlooking small discrepancies.

- To help you work out different scenarios in your business, we’ve compiled a journal entry example for each common transaction.

How confident are you in your long term financial plan?

While the cost of common inventory spoilage may initially be recorded as an asset, it will later be charged to your expenses in a subsequent accounting period. The debit impact of the transaction is a recording of the finished goods in the accounting record, and it remains in the books until sold to the customers. On the other hand, the credit impact of the transaction is a recording of liability or outflow of the cash from the business. Inventory transactions are journalized to keep track of inventory movements. Various kinds of journal entries are made to record the inventory transactions based on the type of circumstance. For example, entries are made to record purchases, sales, and spoilage/obsolescence, etc.

Journal entries in a perpetual inventory system:

When an item is ready to be sold, transfer it from Finished Goods Inventory to Cost of Goods Sold to shift it from inventory to expenses. Debit your Finished Goods Inventory account, and credit your Work-in-process Inventory account. Inventory can be expensive, especially if your business is prone to inventory loss, or inventory shrinkage. Inventory loss can occur if an item or product gets damaged, expires, or is stolen. Before we dive into accounting for inventory, let’s briefly recap what inventory is and how it works.

However, the operational perspective supports the availability of stock in significant quantity. Hence, the business needs to balance between operational and profitability perspectives. In the first stage, inventory is ordered to meet the demand of business operations. The inventory purchased is then processed (known as Work in progress) to produce finished goods.

This entry reflects the acquisition of inventory without the immediate outlay of cash, increasing both the company’s assets (inventory) and liabilities (accounts payable). ABC needs to make journal entry by debiting inventory reserves and credit inventory $ 2,000. SO the company always estimates the inventory write-down and records it into income statement. This entry records the loss from the obsolete inventory and adjusts the inventory account to exclude the value of the outdated items.

For this reason, companies are obligated to select one valuation method and use it consistently over time. Likewise, there is no update to the figures of the cost of goods sold and inventory on October 15, 2020. So, if the company checks the inventory account or cost of goods sold after making the sale of $2,000, it will still show the old figures of the previous period. An accounting journal is a detailed record of the financial transactions of the business.